Most people come to us with the same question: “Should I get term or whole life insurance?” It sounds simple, but the answer can shape your family’s financial future for decades. Pick the wrong type, and you may either overpay for coverage you do not need or end up underprotected when it matters most.

After helping Ohio families navigate life insurance decisions for over 90 years, we know there is no single right answer. There is only the right answer for your situation. This guide will help you find it.

Quick Answer

Term life insuranceprovides affordable protection for a set period (10, 20, or 30 years), ideal for income replacement, mortgage coverage, and raising a family. Whole life insurance covers you for your entire lifetime and builds cash value over time, making it suited for long-term financial planning and estate goals. Most families start with a term; those seeking lifetime security and financial growth choose whole life.

What Is Term Life Insurance?

Term life insurance is exactly what it sounds like: coverage for a defined term, usually 10, 20, or 30 years. If you pass away during that period, your beneficiaries receive the death benefit. If the term ends and you are still living, coverage stops.

Think of it as renting protection for the years when your family needs it most, while your children are young, your mortgage is active, or your income is critical to your household. Term life insurance benefits in the USA make it the most popular starting point for families because it delivers the highest coverage at the most accessible cost. That is not a marketing phrase, is simply how the math works.

Best for: Young parents, homeowners with a mortgage, and anyone who needs significant income replacement coverage during their working years.

What Is Whole Life Insurance?

Whole life insurance is a permanent policy; it does not expire. As long as premiums are paid, your coverage stays active for your entire life. But it does more than just pay a death benefit.

Whole life insurance builds cash value over time. A portion of each premium goes into a savings-like account that grows at a guaranteed rate. You can borrow against this cash value, use it later in life, or let it accumulate as part of your estate.

Whole life insurance, which Ohio families often consider, is not just about protection; it is a long-term financial planning tool. Much like planning for risk with commercial insurance in Ohio, it focuses on stability and long-term value. The cash value component makes it fundamentally different from term coverage, offering both protection and a financial asset you can build over time.

Best for: Those seeking lifelong coverage, individuals focused on estate planning, parents securing final expense coverage, and anyone wanting a policy that builds financial value over decades.

Key Differences Between Term and Whole Life Insurance

Here is a side-by-side life insurance comparison to make the decision clearer:

| Feature | Term Life Insurance | Whole Life Insurance |

| Coverage Duration | Fixed term (10–30 years) | Lifetime |

| Premiums | Lower and fixed for the term | Higher but fixed for life |

| Cash Value | None | Yes grows over time |

| Death Benefit | Paid only if death occurs during the term | Guaranteed payout whenever you pass |

| Complexity | Straightforward | More detailed policy structure |

| Primary Goal | Income and family protection | Protection + financial growth |

| Convertibility | Many policies allow conversion | N/A already permanent |

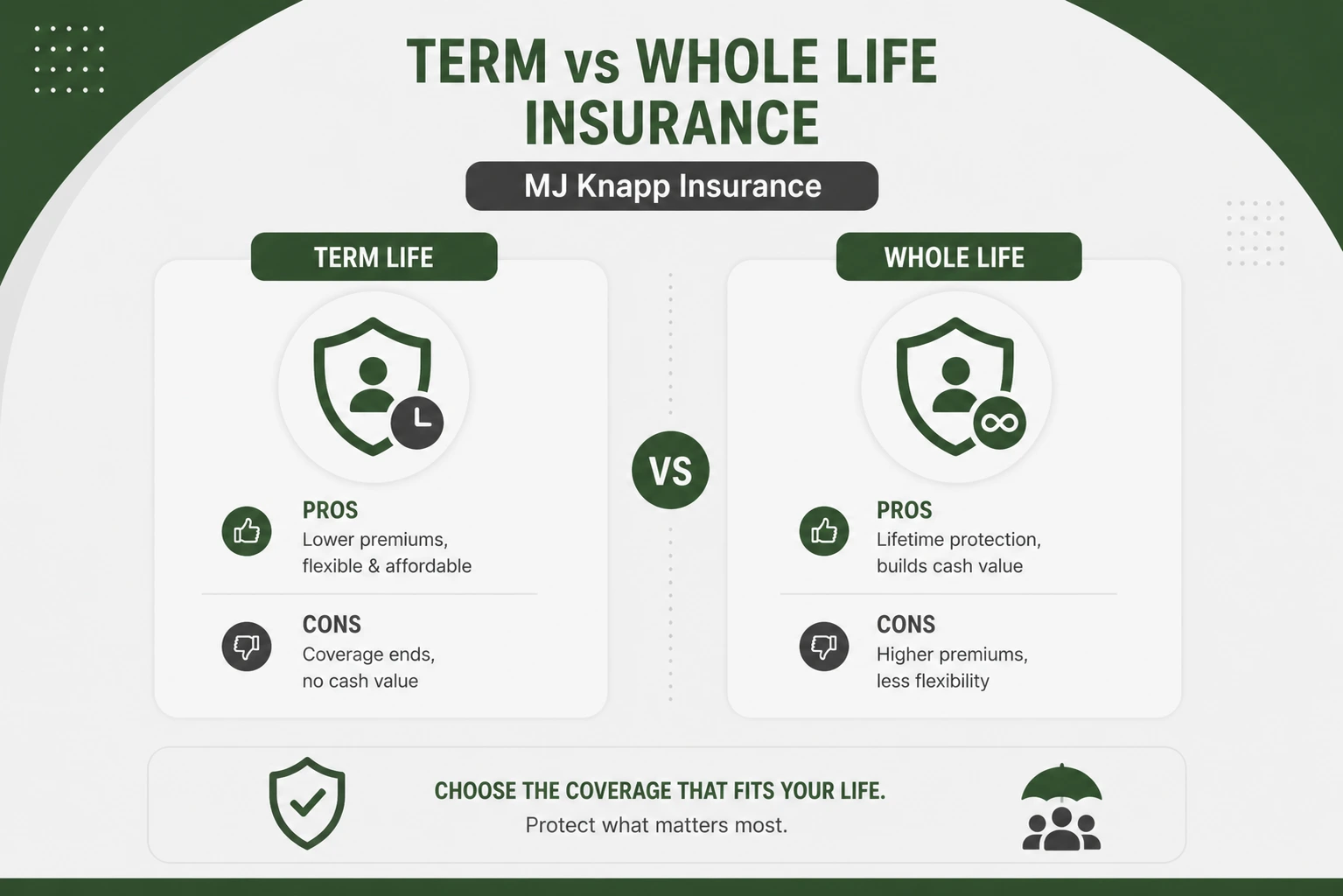

Term vs Whole Life Insurance: Pros and Cons

Every policy type has trade-offs. Here is an honest look at both sides:

Term Life Advantages

- Much lower monthly premiums

- High coverage amounts available

- Simple to understand and manage

- Flexible term lengths to match your needs

- Convertible to permanent coverage

Term Life Limitations

- Coverage ends after the term

- No cash value or savings component

- Renewal can be costly as you age

Whole Life Advantages

- Lifetime protection never expires

- Builds cash value you can access

- Guaranteed death benefit for beneficiaries

- Premiums that never increase

- Useful for estate and legacy planning

Whole Life Limitations

- Significantly higher premiums than term

- Cash value growth is slower than other investments

- Less flexible if financial needs change

Which Life Insurance Is Better for Families?

Here is the real-world question we hear most: “What is best for my family right now?” The answer usually comes down to two things: your current financial stage and your long-term goals.

Choose Term Life If You…

- Have young children who depend on your income

- Carry a mortgage or significant debt

- Need maximum coverage on a budget

- Want a policy that covers your working years

- Are in your 20s, 30s, or early 40s

Choose Whole Life If You…

- Want coverage that never expires.

- Are focused on leaving a financial legacy

- Have maxed out other savings vehicles

- Need coverage for final expenses, guaranteed

- Are you planning for an estate transfer

One thing we tell every client at MJ Knapp: do not let the comparison between term and whole life paralyze you. The best life insurance policy is the one you actually have in place, not the “perfect” one you are still researching.

A Note on Whole Life Insurance Cash Value

This is where most online articles gloss over the details, so we want to be straightforward with you. The cash value in a whole life policy grows at a guaranteed rate set by your insurer. It is not tied to stock market swings, which makes it predictable, but it also grows more slowly than market-based investments over most long periods.

Where cash value becomes genuinely useful is in specific situations: borrowing against it for a large purchase, supplementing retirement income, or ensuring your beneficiaries receive a guaranteed payout no matter what. As an Independent Agent in Ohio, we work closely with clients in Richwood, LaRue, and surrounding communities to walk through these scenarios one-on-one, so the numbers are real, practical, and tailored to your life, not just theoretical.

Understanding this difference is the key to knowing whether whole life insurance is a good fit, or whether a solid term policy paired with separate investments makes more sense for your household.

What Most Misses About This Decision

What they rarely address is the timing question. Many people need term life insurance now, but will benefit from transitioning to permanent coverage later, which is why many insurers build conversion options directly into term policies. You do not have to choose forever. You choose what fits your life today, with the flexibility to adjust as your situation changes.

We have seen clients in their 30s start with affordable term coverage for income protection, then convert or add a permanent policy in their 50s as their focus shifts from raising children to protecting a legacy. That phased approach often makes more financial sense than trying to solve every future scenario with a single policy today.

What Ohio Residents Ask Us Most

“Saved about $500 a year over my previous policy. I had no idea I was overpaying until I came in and compared options”.

Terry D., MJ Knapp client, Richwood, OH

“Incredibly professional and friendly staff. They go all out to find the best deal for their customers, top-notch”.

Dirk M., MJ Knapp client

These are not uncommon outcomes. When a local, independent agency like MJ Knapp compares policies across multiple carriers, clients regularly discover they can either save money on similar coverage or get significantly more protection for what they are already spending.

Term vs Whole Life Insurance for Ohio Residents

If you live in Richwood, LaRue, or anywhere in Marion County, you have the advantage of working with a local advisor who knows this community, not a call center in another state. MJ Knapp Insurance Agency has been helping Ohio families make smart insurance decisions since 1934, and we work with multiple insurance carriers to find you the best fit, not just the easiest sale.

Whether you are comparing life insurance plans in Ohio for the first time or revisiting coverage you already have, a conversation with our team can bring real clarity to what feels like a confusing decision.

Frequently Asked Questions

Q.1 Is term life insurance better than whole life?

It depends on your financial goals. Term life insurance is better for affordable, temporary coverage during your working years, especially if you have dependents and a mortgage. Whole life is better when you need coverage that never expires, want to build cash value, or are planning your estate. Most families find that term fits their immediate needs, with the option to add permanent coverage later.

Q.2 What happens after a 20-year term life policy expires?

When the term ends, coverage stops. Depending on your policy and insurer, you may be able to renew coverage (usually at higher rates because you are older), convert the policy to a permanent plan without a medical exam, or purchase a new policy. It is worth reviewing your options at least a year before your term ends so you are not caught without coverage.

Q.3 Why is whole life insurance more expensive than term?

Whole life insurance costs more because it does two things at once: it provides a guaranteed death benefit for your entire life, and it builds a cash value savings component. You are essentially paying for both permanent protection and a financial growth element. Term insurance only covers a defined period, which is why premiums are significantly lower.

Q.4. Can you convert a term life policy to whole life?

Yes, many term life policies include a conversion option that allows you to switch to a permanent policy without going through a new medical exam. This can be valuable if your health changes during the term period. The availability and terms of conversion vary by insurer and policy, so it is worth confirming this feature when you buy.

Q.5. What happens to whole life insurance when the policyholder passes away?

Your beneficiaries receive the full death benefit, which is guaranteed regardless of when you pass, as long as premiums were paid. Unlike term insurance, there is no expiration date risk. Any accumulated cash value is typically factored into the payout according to your specific policy structure.

Q.6. What type of life insurance is best for families in Ohio?

For most Ohio families, term life insurance is the most practical starting point because it delivers strong income protection and mortgage coverage at a manageable monthly cost. Whole life insurance becomes a better fit as financial goals shift toward wealth preservation and estate planning. An independent agent can compare options across multiple carriers to find what truly fits your household, which is exactly what MJ Knapp Insurance Agency has done for Marion County families since 1934.

The Bottom Line

When you compare term vs whole life insurance side by side, the differences become clear, but the right choice is still personal. Term life insurance offers strong, affordable protection for the years when your family depends on you most. Whole life insurance offers lifetime coverage with a financial growth component for those thinking decades ahead.

The worst decision is no decision. If your family would struggle financially without your income, the right time to secure life insurance coverage is now, not after more research.

At MJ Knapp Insurance Agency, we have been helping Richwood, LaRue, and Marion County families make exactly this decision since 1934. We work as an independent agency, which means we compare options from multiple carriers on your behalf, always aiming for the best value, not the easiest commission.

If you are ready to compare life insurance policies and want straightforward guidance from people who know this community, reach out to our team or visit us at 6 S Franklin St, Richwood, OH 43344.